Evaluating risk in hard tech

Fantastic risks, and where to find them.

In Aesop’s fable ‘The Fox and the Grapes,’ a fox, unable to reach some appealing grapes at the top of a tree, convinces himself they are sour, unworthy of pursuit.

Just like in the fable, there’s a prevailing narrative that I’ve touched on before but it bears repeating: the risks associated with deep/hard tech are often misjudged compared to those in software businesses.

“Silicon Valley […] is built to fund software companies and the further away you get from that software core, the less reliable it is as a funding mechanism”, Michael Seibel, Lessons from thousands of startups

Decades of software investing will have that effect. Investors have become reluctant to fund startups that require any form of hardware to operate. And Silicon Valley has engineered a generation of investors that does not know, for the most part, how to underwrite hardware first businesses. It’s high time to reassess how we evaluate these risks. And secure those grapes, especially given the density and quality of companies bringing a new hard tech renaissance to life.

In this post, I attempt a clarification of the risk-evaluation framework needed to evaluate and ultimate fund more early-stage hardware businesses.

Thinking like an investor: Risk underwriting and visualization

At its most fundamental level, the job of a venture capitalist is to invest in assets that rightly rewards the risk being taken. It’s a very straightforward application of modern portfolio theory, as the produced portfolio seeks to maximize the expected level of return for a given level of risk.

When investors say “hardware is too complicated”, they mean that the risks associated with it are too difficult to understand to justify the potential outcome.

Unfortunately, too much capital stays on the sidelines when these companies reach VC inboxes.

The thing is, the next generation of great companies will be built with atoms, not just bits. Most deeptech and climate startups rely on hardware at some point in their product.

Effective fundraisers have mastered the art of risk framing, demonstrating the ability to clearly articulate the risks associated with each milestone. And then, reassure the investors on how they will meet each one of them. In return, investors have developed standardized expectations for each round of fundraising.

In that context, the onion theory emerged as a simple method to clarify the steps in the progression path of a software startup. Marc Andreessen popularized it through his talk on the topic, crediting the idea to Andy Rachleff of Benchmark.

I won’t expand on the onion theory itself, but it roughly follows the following sequential steps:

- Team Risk: Is the team capable of executing their vision? Will the team work together effectively?

- Building Risk: Can they develop a viable product?

- Market Risk: Is there a substantial market for the product? Will customers use and pay for it?

- Go-To-Market Risk: Can they effectively market and sell the product? Will the launch go well?

- Competition Risk: Can the company prevail against competition?

The theory aims to bring a sense of predictability and linearity in an information-starved decision making exercise. It introduces systems to an inherently chaotic process, helping investors sleep at night and founders find a sense of direction to allocate these ressources. It also delivered standardization to both investors and the founders pitching them at each funding round.

As a founder, the goal then becomes to metaphorically peel each layer of the onion — Each fundraising milestone turning into a set of risks being evaluated and sidelined. The earliest investors become the partners to help figure out what to focus on. Good pre-seed angels and investors are often described as “having taste” for good startups — In truth, it mostly means that they do a good job understanding the derisking process to reach the next round. Even a software startup valuation becomes, in large part, the output of the amount of capital needed to write-off the next set of risk(s).

This theory results in a fairly clear set of expectations at each stage of fundraising: A software startup gearing up for a Series A fundraise knows that it will need to show a proven PMF with a clearly defined ICP, early proofs of a repeatable sales strategy, and a capacity to recruit 2–3 high level IC talents in their product team.

There is no reason why we can’t bring the same level of clarity to hardware. Indeed, to help guide more capital into hard tech startups, we must adapt and refine our risk assessment tools to offer the same clarity for hardtech as we’ve achieved with software.

By doing so, we can unlock the potential of a sector that, data from investors like Leo Polovets of Humba suggests, might yield returns comparable to software, given the right understanding and framework. Apple, for instance, only raised $3.5M by the time it went public in December 1980 at $271M. Not a bad equity to capital raised ratio.

Adapting the onion theory to hard tech:

In the perennial comparison between hardware and software — which itself is questionable: A HaaS business will look more similar to software, financially speaking, than a FOAK factory — the distinctions often boil down to their fundamental business models and market dynamics. While software continues to revel in its scalability and low marginal costs, hardware presents a different set of challenges and opportunities that are equally compelling.

Here is how we could grossly summarize the differences between hard tech and software:

Easier Aspects of Hard tech:

- Less Competition: Hardware startups face fewer immediate competitors, which can be attributed to higher entry barriers and the complexity involved in product development.

- Long-Term Defensibility: Due to the physical and technical complexities, hardware innovations are harder to replicate, providing stronger defensibility against incumbents who might rather acquire than innovate.

- Market Dynamics: The hardware sector tends to move at a slower pace, making it easier to time market entry. Large players often validate new technologies through acquisitions, partnerships, or investments.

- Easier partnerships: A higher willingness to co-develop from potential clients.

- Diversified financing sources: The existence of tangible assets makes hardware businesses easier to financialize. As opposed to software which is mostly limited to equity fundraising and venture debt.

Challenging Aspects of Hardware:

- Talent Density: Finding the right talent with the necessary expertise in hardware is often more challenging than in software.

- Flexibility and Pivots: Hardware development does not easily lend itself to pivots. Once a product design is set and manufacturing begins, making changes can be costly and time-consuming.

- Profitability and Timing: Hardware companies may remain unprofitable for longer periods, dependent on precise timing for market readiness and adoption.

- Marginal cost of goods: Each additional unit of revenue is virtually cost less in software. Hardware companies have COGS that will hover between 20% to 50% of revenue.

What doesn’t change much, surprisingly, are the historical success rates and capital needs to achieve a venture scale outcome (roughly defined as a standard $1B+ outcome).

Shaun Abrahmson of Third Sphere sums it up nicely in his comparison of software and hardware companies total equity raised vs. IPO value. On average (excluding generational outliers like Google or Nvidia), the efficiency of a Dropbox-like software company is relatively similar to that of a hardware company.

Front-loading vs. back-loading risk

Instead of using growth efficiency as the number one metric, a better way to view this difference lies in the tradeoff between tail-end risk for early risk. Software risk is more present on the tail-end due to the low cost of growth and ease of building a sellable MVP, as well as the access to talent and playbooks. After all, we’re more likely to be funding the end of the software cycle. This effectively decreases barriers to entry, and therefore the total aggregated value of a software business over its lifetime. Many public software companies might never achieve profitability due to limited competitive moats, eroding margins, and inefficient middle management.

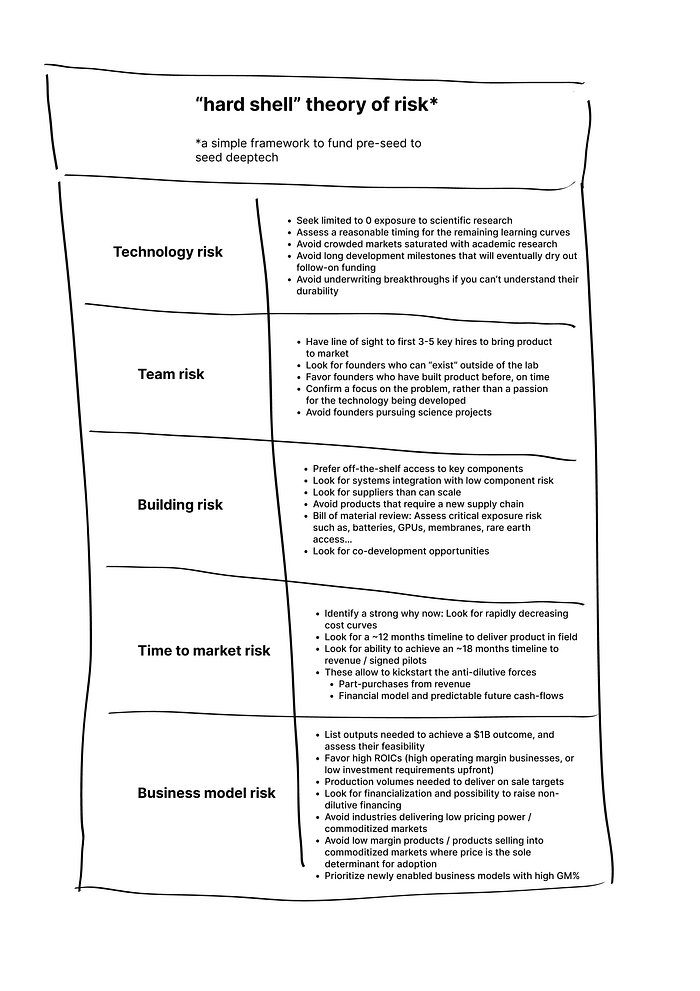

Finding the right model: The “hard shell” theory of risk

To more accurately assess the risks associated with hardware, it is essential to adopt a model of evaluation that accounts for these variations in the distribution alongside the progression path.

Technical risk needs to be better understood and largely solved for early on into the life of the company. Given the need to rapidly switch to a financial model, the technical risk taken cannot (1) delay the revenue generation beyond 24 months and (2) remain largely reliant on research and learning curves. If it isn’t the case, the revenue generation cannot happen soon enough to unlock the partnerships and early pilots needed to survive the Series B drought.

The best performing hardware investments therefore tend to mostly bring systems engineering to the equation, assembling “known technologies” in novel ways, rather than creating entirely new ones.

The risk evaluation model also needs to go beyond technical risk to include the aspects of financialization that are required to offset the early dilution incurred. Despite this, it’s important to not just see it as a downside.The unique aspect of hard tech is that the significant dilution occurring in the early funding rounds often unlocks greater financing capabilities later and durable MOATs. Indeed, a staggering 49% of companies in climate, space, agriculture and quantum have received government funding.

The singular goal for those companies is to reach the inflection point where it becomes the only one capable of solving a deeply entrenched pain point at a marginally lower cost than the previous alternative. Financing, recurring high margin business contracts and product expansion with high defensibility is much more likely to happen after that point is unlocked.

This is why I propose a different theory of risk for early-stage hard tech startups. Think of the hard tech risks as a tough shell — a shell that’s hard to crack but, once penetrated with the right insight, reveals invaluable opportunities (the juicy part). The initial breakthrough, proving the core technology can be scaled and financed, is the toughest challenge but also the most rewarding.

— —

Below is a first attempt at describing the “hard shell” layer of risk mitigating factors to underwrite early hard tech teams. I’d love to hear and integrate your comments, so here’s a working draft link.

— Julien